Have you ever felt like you’re constantly spending money, but can’t quite pinpoint where it’s all going? I know I have! In today’s economy, it’s a common struggle. We’re bombarded with new products, services, and experiences, and it can be hard to resist. The latest US consumer spending reports are out, and they paint a picture of just how much things are changing. Are we spending more, saving less, or is it a bit of both? Let’s dive into the data to find out what’s really happening with our money. 😊

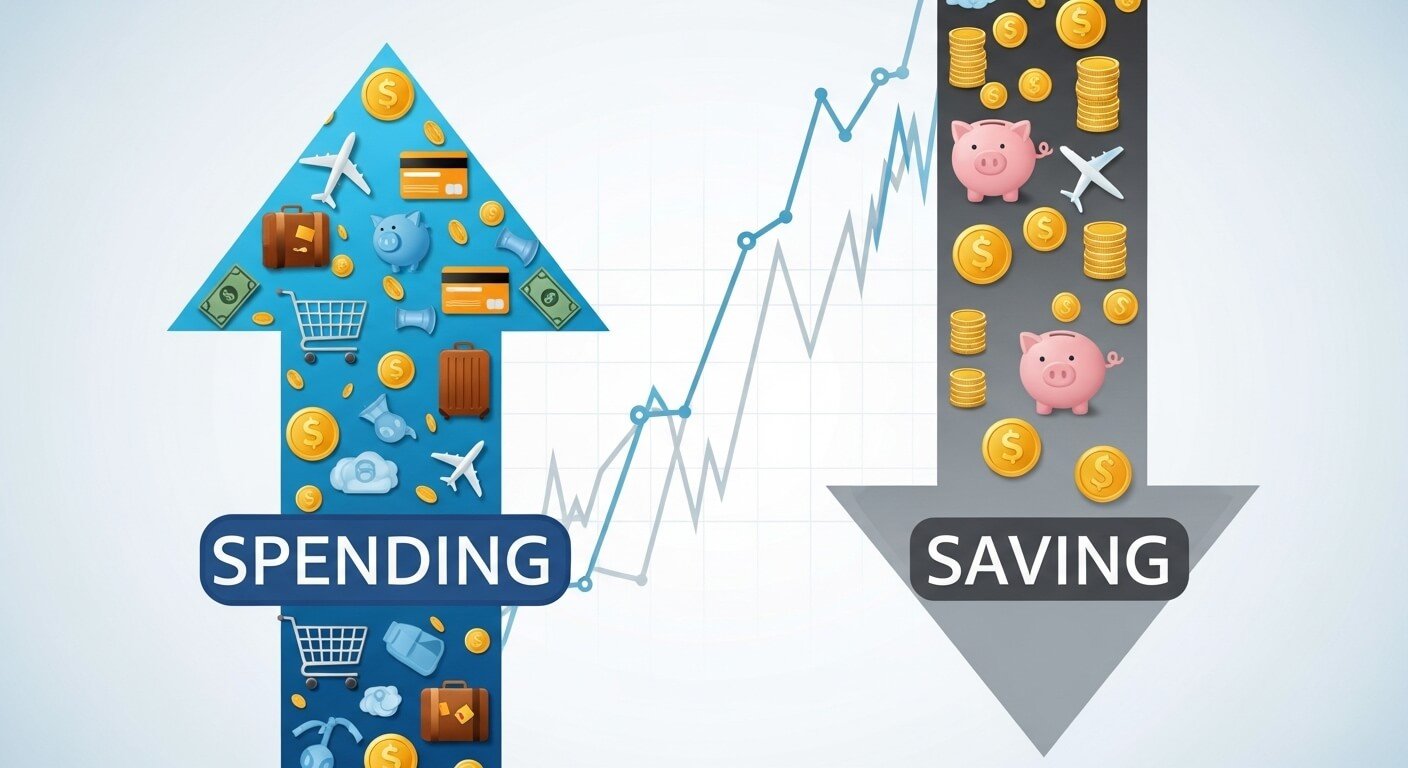

The Big Picture: Spending vs. Saving Trends 🤔

At a high level, the data from recent quarters shows a clear trend: consumer spending continues to rise, while the personal saving rate is on a downward trajectory. This isn’t just about inflation; it reflects deeper changes in how households are managing their finances. We’re seeing increased spending on everything from travel and dining to durable goods and new technologies. This is happening even as economic uncertainty looms for some.

This shift isn’t a new phenomenon, but its pace has accelerated. For a long time, the prevailing wisdom was to save as much as possible for a rainy day. Now, with a strong job market and a desire to make up for lost time from the pandemic, many people are prioritizing experiences and immediate gratification over long-term savings. It’s a complicated trade-off, and one that has big implications for individual financial health.

What’s Driving the Change? 📊

So, what’s causing this shift? It’s a mix of different factors, both economic and psychological. On the economic front, a robust labor market means more people have disposable income. At the same time, inflation has made everything from groceries to gas more expensive, forcing households to spend a larger portion of their income just to maintain their standard of living. This has squeezed saving rates, even for those with higher earnings.

Beyond economics, there’s a real change in consumer mindset. Think about the rise of “revenge spending” post-pandemic. People were cooped up for so long that they’re now eager to travel, dine out, and attend events. This desire for experiences is powerful, and it’s reflected in the data. Spending on services like hospitality and entertainment has seen a particularly sharp increase. This is why you see things like concert tickets and travel packages selling out so quickly.

Key Spending Trends in Q3 2025

| Category | Spending Change (YoY) | Impact on Savings |

|---|---|---|

| Services (Travel, Dining) | Strong increase | Significant decrease in discretionary savings |

| Durable Goods (Appliances, Cars) | Moderate increase | Requires large one-time expenditures, impacting liquidity |

| Non-Durable Goods (Groceries, Gas) | Price-driven increase | Reduces overall saving capacity |

Navigating Your Finances 🧮

So, what does this all mean for you and your wallet? It’s easy to get caught up in the spending wave, but a little bit of planning can make a huge difference. The key is to find a balance between enjoying life now and securing your financial future. This isn’t about giving up everything you love, but about making smart, intentional choices.

📝 The 50/30/20 Rule: A Simple Guide

Budget = Needs (50%) + Wants (30%) + Savings (20%)

Here’s a quick breakdown of how to apply this rule to your own budget:

- Needs (50%): Housing, utilities, groceries, and transportation. These are non-negotiable expenses.

- Wants (30%): Dining out, entertainment, subscriptions, and hobbies. This is where your fun money goes.

- Savings & Debt (20%): This includes contributions to your savings account, retirement funds (like a 401k), and paying down debt.

🔢 Simple Budget Calculator

Enter your monthly take-home pay to see a quick budget breakdown.

The Long-Term Impact 👩💼👨💻

It's not just about today's budget; it's about what these trends mean for our financial futures. A low savings rate can make us more vulnerable to economic shocks, like job loss or unexpected expenses. It also means we might be missing out on the power of compounding interest, which is a major key to wealth building.

The good news is that small changes can make a big difference over time. Even saving an extra 1% of your income each month can accumulate significantly, especially if you invest it wisely. The key is consistency and discipline. As we continue to see reports on consumer spending, remember that each choice you make, big or small, contributes to your own financial story.

Wrapping Up: What You Need to Know 📝

Ultimately, the data shows that Americans are indeed spending more and saving less. This is driven by a mix of inflation, a strong job market, and a desire for post-pandemic experiences. While this isn't necessarily a bad thing in moderation, it's a trend that could lead to financial vulnerability if not managed wisely. By adopting a disciplined approach to budgeting and prioritizing saving, you can take control of your financial future.

Consumer Spending Report: Key Takeaways

Frequently Asked Questions ❓

Thanks for reading, and I hope this helps you navigate your financial journey. If you have any more questions, feel free to ask in the comments! 😊