🚨 Palantir Stock Analysis: The “Insider” Audit

- SBC Addiction: They claim to be profitable, but they are paying employees with massive amounts of stock. This creates constant dilution for existing shareholders. It’s a wealth transfer from you to them.

- Valuation Vertigo: Trading at a P/E ratio in the hundreds. The stock is priced for “World Domination,” meaning any slight miss in growth will cause a crash.

- Insider Selling: While CEO Alex Karp hypes the AI revolution on TV, insiders are quietly selling shares. Follow the money, not the mouth.

Executive Summary: A Great Charity for Employees

I will give credit where credit is due: Palantir Technologies (PLTR) builds incredible software. Their “Gotham” and “Foundry” platforms are genuinely best-in-class.

But here is the hard truth that fanboys ignore: A great product does not always make a great stock.

My forensic Palantir stock analysis reveals a company that operates less like a shareholder-friendly corporation and more like a massive welfare fund for its engineers and executives. You are buying the stock, but they are taking the profits home via stock-based compensation.

The Audit: Why PLTR is a Trap

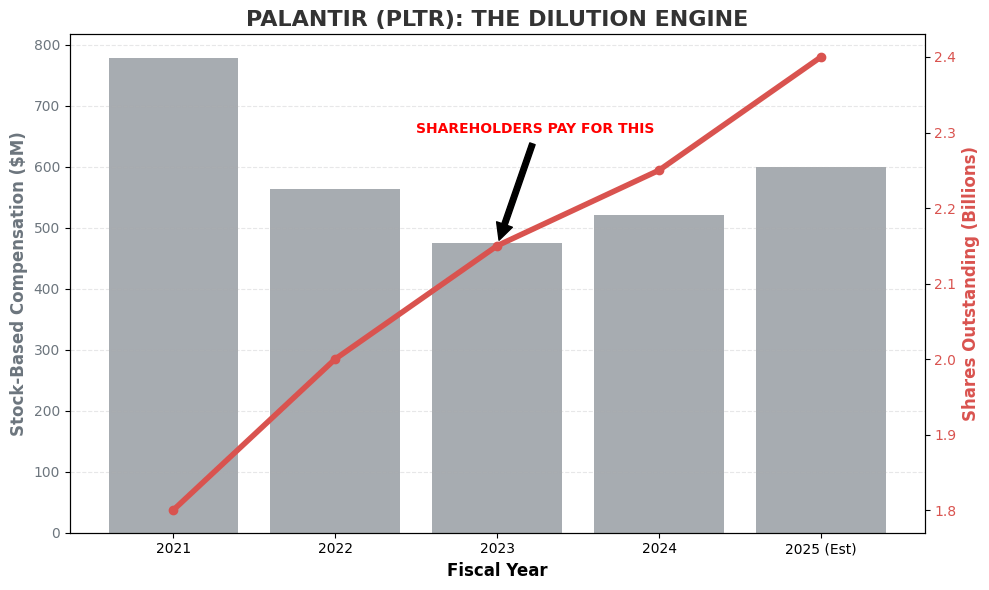

1. The Dilution Machine (Stock-Based Compensation)

Palantir loves to talk about “Adjusted Free Cash Flow.” Why? Because it allows them to ignore the massive cost of Stock-Based Compensation (SBC).

Instead of paying cash bonuses, they print new shares and give them to employees. This increases the total number of shares (supply), which makes your shares (demand) worth less. It is invisible inflation.

Look at the chart below. The bars represent the massive value being transferred to employees, while the red line shows the swelling share count.

2. Valuation Vertigo: Priced for Perfection

Palantir is currently trading at a P/E (Price-to-Earnings) ratio that rivals or exceeds Nvidia. But unlike Nvidia, Palantir is not doubling its revenue every quarter.

| Metric | Palantir (PLTR) | Sector Avg | Forensic Note |

|---|---|---|---|

| P/E Ratio | 150x ~ 200x+ | 25x | Priced as if it has already won. |

| P/S Ratio | 25x+ | 6x | Extremely expensive revenue. |

At these levels, the stock is extremely fragile. Any news that is “good but not great” could trigger a massive sell-off. You are picking up pennies in front of a steamroller.

3. Insider Selling: Actions Speak Louder

If the future is so bright, why are they selling?

Check the SEC Form 4 filings. Executives and insiders have been consistent sellers of the stock. CEO Alex Karp sells huge blocks of shares regularly. While they tell retail investors to “hold for the long term,” they are cashing out now.

Rule of Wall Street: When the Chef doesn’t eat his own cooking, you should probably leave the restaurant.

The Verdict

HOLD / TRIM (High Risk)

Palantir is a real company with real tech, unlike the scams we usually analyze. However, the Stock is disconnected from the Company.

This stock is currently structured to enrich employees through SBC, not you. If you own it, consider taking profits. If you don’t own it, wait for the inevitable crash to a realistic valuation.