🚨 MSTR Warning: The “Leverage” Audit

- The “Shell” Company: The actual software business is dead money. Revenue is stagnant. The only thing keeping this ticker alive is Bitcoin speculation.

- Debt-Fueled Gambling: They are issuing billions in Convertible Notes to buy crypto. This is not investing; it is leveraging the entire company on a single, volatile asset.

- One Crash Away from Ruin: If a “Crypto Winter” hits, the value of their assets collapses while the debt remains. MSTR is a ticking time bomb.

Executive Summary: Michael Saylor’s Casino

Let’s stop pretending MicroStrategy (MSTR) is a tech company. It is a hedge fund run by a Bitcoin maximalist, disguised as a software firm.

Buying MSTR stock is not investing in innovation. It is buying a leveraged bet on Bitcoin, but with the added risk of massive corporate debt and management fees. Michael Saylor has turned a boring software company into a high-stakes casino. And in this casino, he is betting borrowed money.

The Audit: Why MSTR is a House of Cards

1. Stagnant Core Business: The Empty Shell

Before Bitcoin, MicroStrategy was a mediocre Business Intelligence (BI) company losing market share. After Bitcoin? It’s still a mediocre BI company.

The Income Statement shows that the core operations are barely keeping the lights on. Operating income from software is flat or declining. They have abandoned the idea of growing the business in favor of financial engineering. The company is now just a wrapper for a crypto wallet.

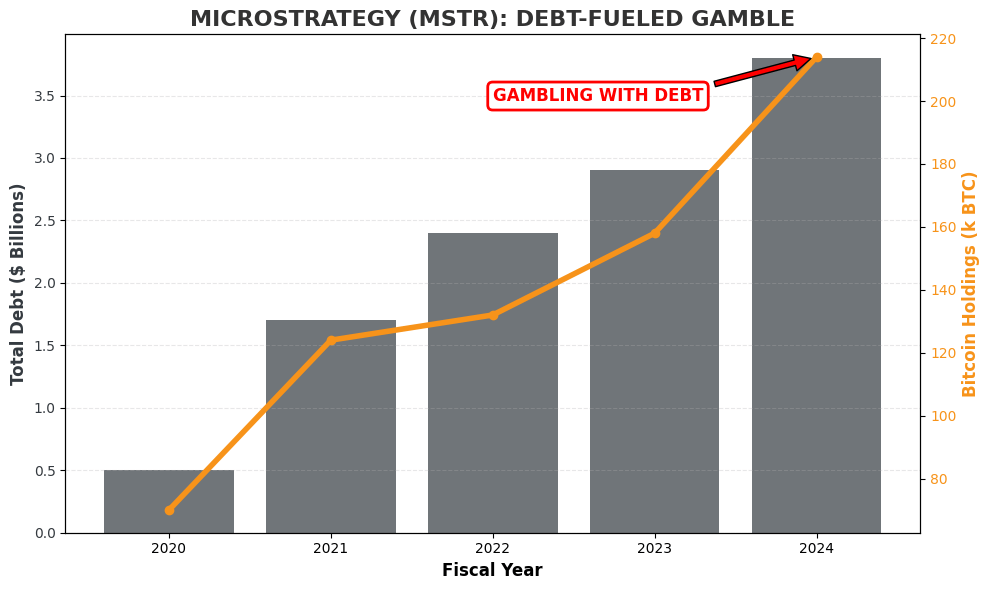

2. Debt-Fueled Gambling: The Leverage Trap

How do you buy 200,000+ Bitcoins when your business doesn’t generate enough cash? You borrow it.

The Balance Sheet is loaded with Convertible Notes. They are borrowing from the future to speculate today. If Bitcoin price goes up, they look like geniuses. If Bitcoin crashes, they are left with massive interest payments and assets worth a fraction of the debt.

The chart below visualizes this dangerous correlation:

3. Distorted Assets: The Volatility Nightmare

A normal company has assets like factories, patents, or cash. MSTR has “Digital Assets.”

📊 Forensic Data: The Balance Sheet Risk

| Metric | Status | Forensic Note |

|---|---|---|

| Asset Concentration | ~90% Crypto | Zero diversification. All eggs in one volatile basket. |

| Impairment Risk | Extremely High | If BTC drops 10%, they book hundreds of millions in losses. |

| Core Revenue | Stagnant | The actual business is effectively a zombie. |

This accounting structure means MSTR’s earnings are meaningless. They fluctuate wildly based on crypto prices, not business performance. It is impossible to value this company using traditional metrics.

The Verdict

HIGH RISK / SPECULATIVE

If you want to own Bitcoin, buy Bitcoin. Do not buy a debt-laden software company that owns Bitcoin.

MSTR is a “Leverage Monster.” In a bull market, it flies. In a bear market, it dies. Don’t let Michael Saylor gamble with your life savings.