💳 Detective’s Briefing: The Debt Matrix

- The Invention: The **FICO Credit Score** is not a government program. It is a product invented in 1989 by a private company (Fair Isaac Corporation) to sell your data to banks.

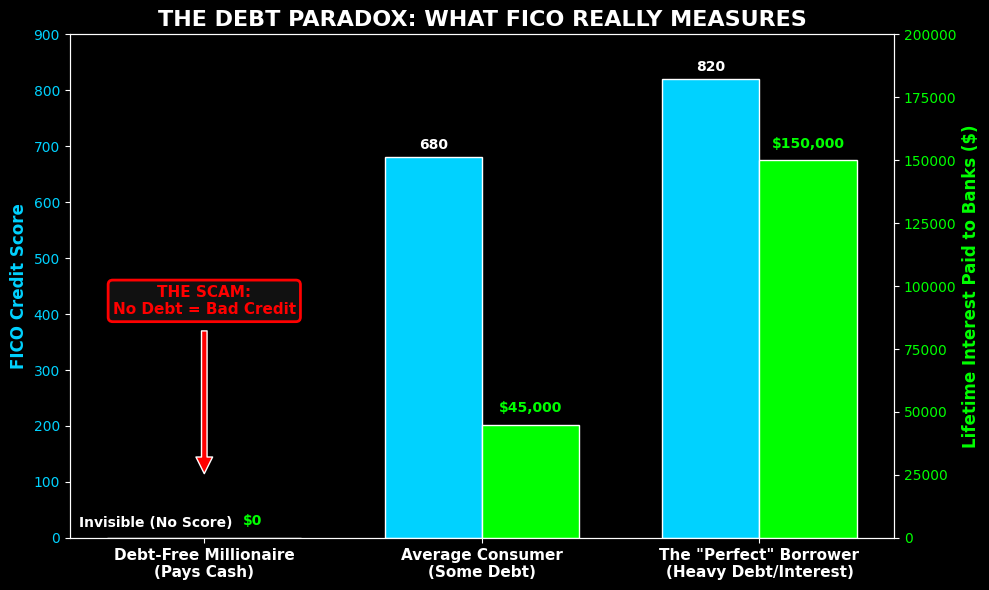

- The Paradox: If you are a billionaire who pays for everything in cash and has zero debt, you are “Credit Invisible.” The score measures your *profitability* to banks, not your wealth.

- The 2026 Surveillance (FICO 10T): The new algorithm tracks your rent, utilities, and “Buy Now, Pay Later” (BNPL) apps, pulling every aspect of your life into the debt matrix.

We are taught from a young age that achieving a perfect 800 **FICO Credit Score** is the ultimate sign of financial responsibility. You check it on your banking app. You stress when it drops 5 points.

But what if the entire system is a rigged game? What if the score you are trying so hard to protect is actually a measure of how good of a slave you are to the banking system?

In this investigation, we peel back the curtain on the most successful psychological trick in modern capitalism, and expose the monopoly that collects a toll every time you borrow money.

The 1989 Invention: A Measure of Debt, Not Wealth

Most people assume the **FICO Credit Score** is a government-backed metric that measures your overall financial health.

It is not. It was invented in 1989 by the Fair Isaac Corporation.

Here is the shocking paradox of the system: Your income, your savings account, and your stock portfolio do not matter to FICO. They are not part of the calculation.

The “Credit Invisible” Billionaire

Imagine a millionaire who hates debt. They buy their cars in cash, buy their house in cash, and use a debit card for groceries. Because they do not borrow money and pay interest, the FICO system classifies them as “Credit Invisible.” They effectively have a score of zero.

Meanwhile, a person living paycheck to paycheck, carrying a $10,000 balance on three different credit cards but making the minimum payments on time, will have a score of 750+.

The score does not measure if you are rich. It measures how profitable you are to lenders without defaulting.

The 2026 Surveillance: The FICO 10T Update

The system is getting hungrier. Historically, the **FICO Credit Score** only looked at traditional debt (mortgages, credit cards, auto loans).

But the new generation (Gen Z) relies heavily on “Buy Now, Pay Later” (BNPL) apps like Affirm and Klarna, or debit cards. To capture this, the Federal Housing Finance Agency (FHFA) approved the transition to the new FICO 10T model.

No Escape from the Matrix

FICO 10T incorporates “trended data.” It tracks your rent payments, your utility bills, your cell phone bills, and your BNPL history.

They spin this as “helping people with thin credit files.” In reality, it is pulling every single daily transaction you make into the surveillance matrix. You can no longer fly under the radar. Every move you make is scored and monetized.

The Detective’s Verdict: Own the Tollbooth

While millions of consumers stress over their scores, the creators of the system are getting rich.

Fair Isaac Corporation is a B2B monopoly. Every time you apply for a credit card, an auto loan, or a mortgage, the bank pays FICO a small fee to pull your score. It is a literal tollbooth on the American economy.

📊 The “Debt Matrix” Portfolio

| Ticker | Company | The Logic |

|---|---|---|

| $FICO | Fair Isaac Corp. | They own the algorithm. Pricing power is absolute. Banks cannot issue mortgages without paying FICO. A flawless monopoly. |

| $V / $MA | Visa / Mastercard | The highways of debt. They don’t take the credit risk; they just take a 2% cut of every swipe in the debt economy. |

DON’T PLAY THEIR GAME

The **FICO Credit Score** is designed to keep you on the treadmill of debt. If you play the game, you make the banks rich.

Stop trying to impress a 1989 algorithm. Focus on your net worth, not your debt score. And if you want to win, buy the company that owns the algorithm ($FICO).