Key Takeaways (TL;DR)

- China is Bleeding Out: iPhone revenue is flatlining, and China sales dropped 4%. This isn’t a slump; it’s an exodus.

- The Buyback Ponzi: Apple is burning $110B annually to artificially inflate EPS. They aren’t innovating; they are deleting shares.

- Services on Quicksand: You cannot grow Services revenue when your hardware user base is shrinking.

Executive Summary: The World’s Most Expensive Bank

Stop calling Apple a technology company. It was a tech company under Jobs. Under Cook, it has morphed into a glorified hedge fund that happens to sell glass rectangles.

The “Apple Stock Forecast 2025” narrative being pushed by mainstream media is filled with fluff about AI integration. As a forensic accountant, I look at the cash flow. The data screams one thing: Apple has stopped growing. Instead, they are cannibalizing their own balance sheet to keep the stock price on life support.

The Audit: Rotting at the Core

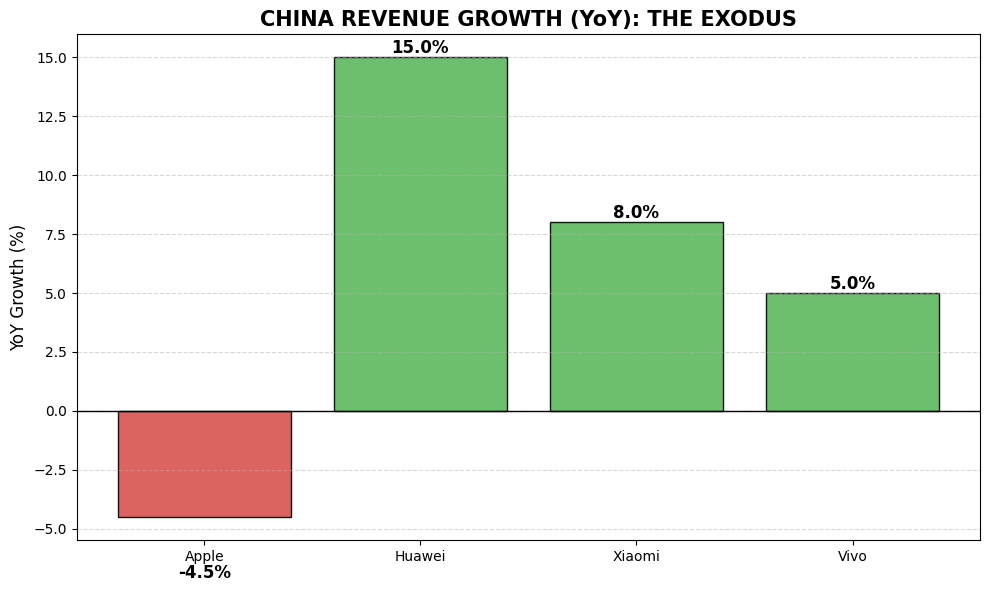

1. The China Crisis: A Hemorrhage, Not a Scratch

For years, the bull case for Apple hinged on the Chinese middle class. That dream is dead. While domestic competitors like Huawei are surging with double-digit growth, Apple is seeing red.

The chart below exposes the reality regarding market share momentum:

- Revenue Stagnation: iPhone revenue has been stuck at the $200 billion ceiling for years. There is no organic growth here.

- Market Share Collapse: In China, Apple’s revenue dropped by over 4% YoY, falling to 3rd place.

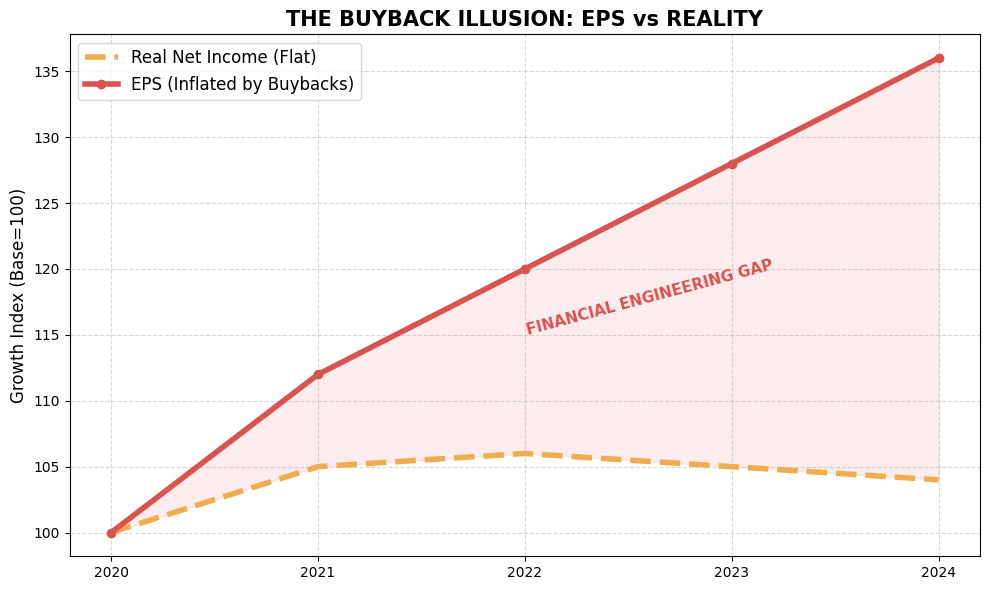

2. The Buyback Illusion: $110 Billion in Smoke and Mirrors

This is the ugliest part of the balance sheet. Apple is authorizing $110 billion in share buybacks annually. They are effectively admitting they have no R&D ideas worth investing in, so they are pumping the stock price instead.

| Metric | The Reality | Forensic Interpretation |

|---|---|---|

| Annual Buyback | $110 Billion | Artificial price inflation. |

| Real Net Income | Stagnant / Flat | Business is stalled. |

| EPS (Earnings Per Share) | Rising | FAKE. Driven by share reduction, not sales. |

Look at the gap in the chart below. This is what we call “Financial Engineering.”

3. The “Services” Myth: A Castle Built on Sand

Bulls love to talk about Apple Services (iCloud, Apple Music, App Store) as the savior. They argue that even if hardware fails, software will win. This is delusional logic.

Hardware is the gateway drug. If people stop buying iPhones—which the data shows they are—the subscriber funnel dries up. You cannot have a thriving Services business with a shrinking hardware user base. It is a lagging indicator.

The Verdict

SELL / AVOID

Apple is no longer an innovation company. It is a massive bank that uses its cash pile to manipulate its own stock price. The “growth” you see is a mirage created by $110 billion in buybacks.

With China turning its back on the iPhone and no groundbreaking hardware in the pipeline, the fundamentals are toxic. This wallet is full of dust.

Disclaimer: The content provided in this article is for informational purposes only. The author is not a licensed financial advisor. The views expressed here are those of the author based on forensic analysis of public data. All investments involve risk. Do your own due diligence.